NI PUB, NI SPONSOR, NI SUBVENTION, SEULEMENT VOUS ET NOUS....SOUTENEZ CE BLOG FAITES UN DON

NI PUB, NI SPONSOR, NI SUBVENTION, SEULEMENT VOUS ET NOUS....SOUTENEZ CE BLOG FAITES UN DON

Risky Asset Outflows Surge Again As “Up-In-Quality” Rotation Accelerates

Market weakness, as BofAML reports, has taken a toll on mutual fund and ETF flows, with stocks (-$9.56bn), HY bonds (-$1.56bn) and levered loans (-$1.17bn) all reporting significant outflows last week (ending on October 1st). There is a clear “up in quality” and “up in capital structure” rotation among investors as investment grade bonds saw huge inflows. Notably, most PIMCO funds, including the Total Return Funds, do not report flows weekly, and hence the bulk of this outflow was not reflected in the last week’s data. In a statement PIMCO said that outflows from the Total Return Fund totaled $23.5bn in September, so we will have to see just where that outflow hit.

Risk-off…

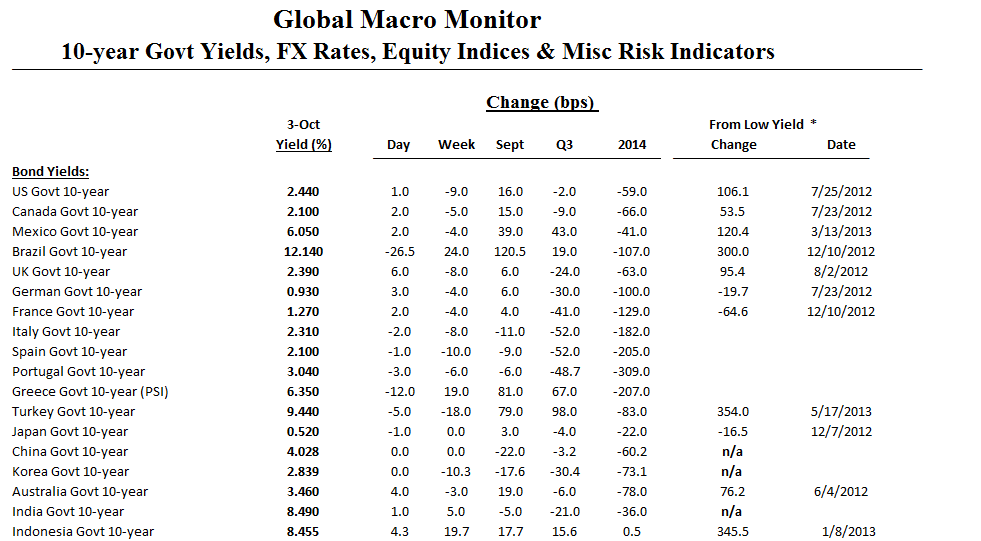

Click on table to enlarge and for better resolution

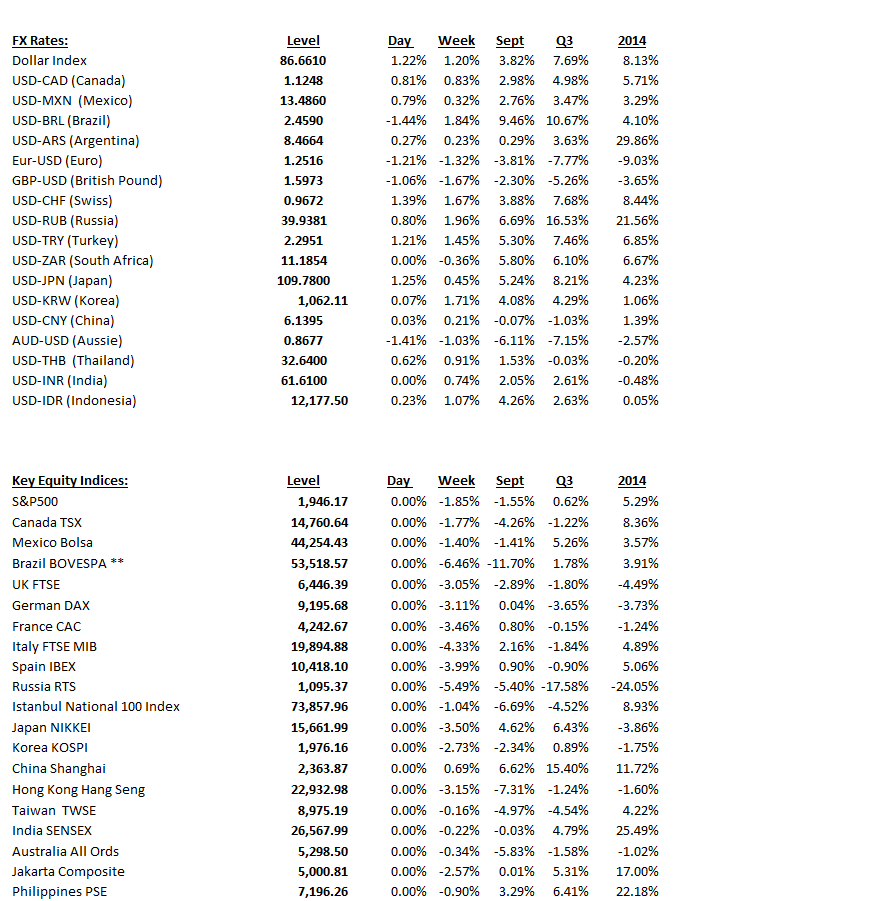

(click here if table is not observable)

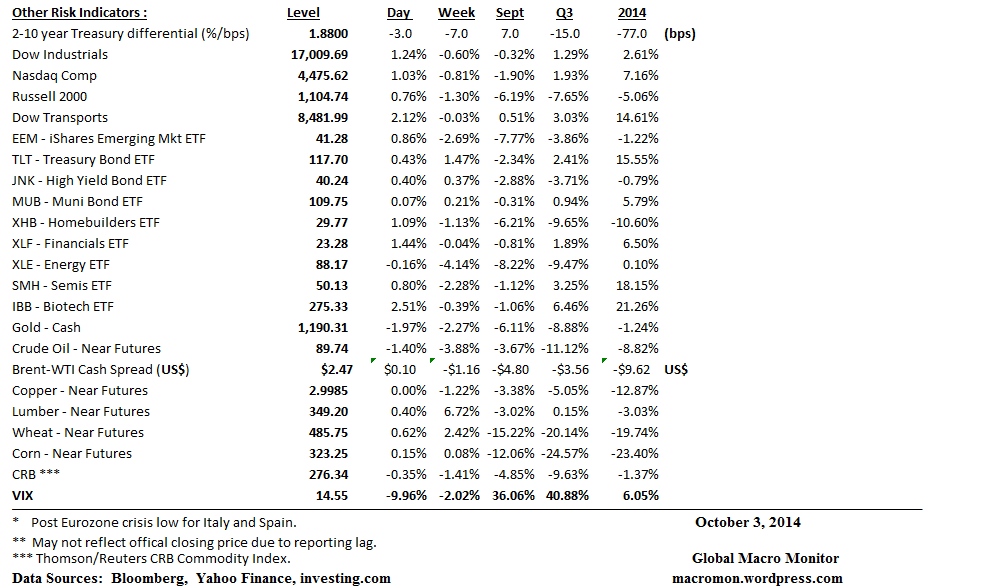

(click here if table is not observable)

En savoir plus sur Le blog A Lupus un regard hagard sur Lécocomics et ses finances

Abonnez-vous pour recevoir les derniers articles par e-mail.